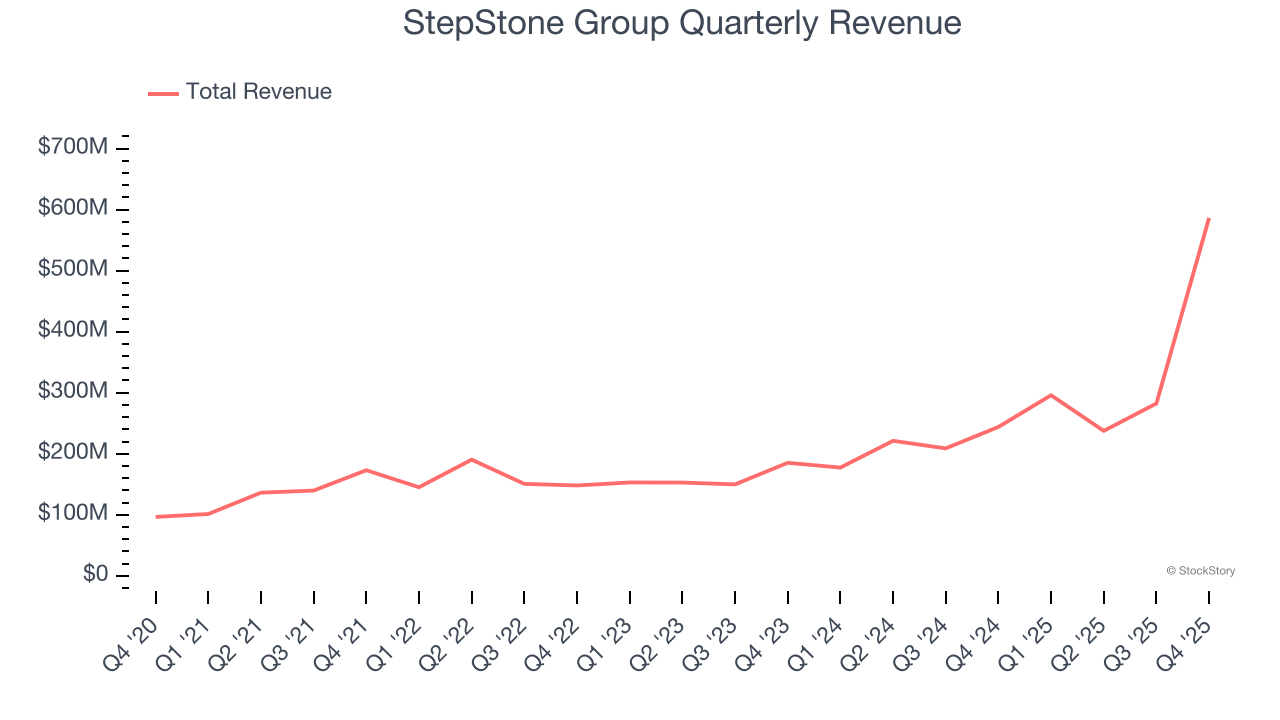

Private markets investment firm StepStone Group (NASDAQ:STEP) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 140% year on year to $586.5 million. Its non-GAAP profit of $0.65 per share was 4.7% above analysts’ consensus estimates.

Is now the time to buy StepStone Group? Find out by accessing our full research report, it’s free.

StepStone Group (STEP) Q4 CY2025 Highlights:

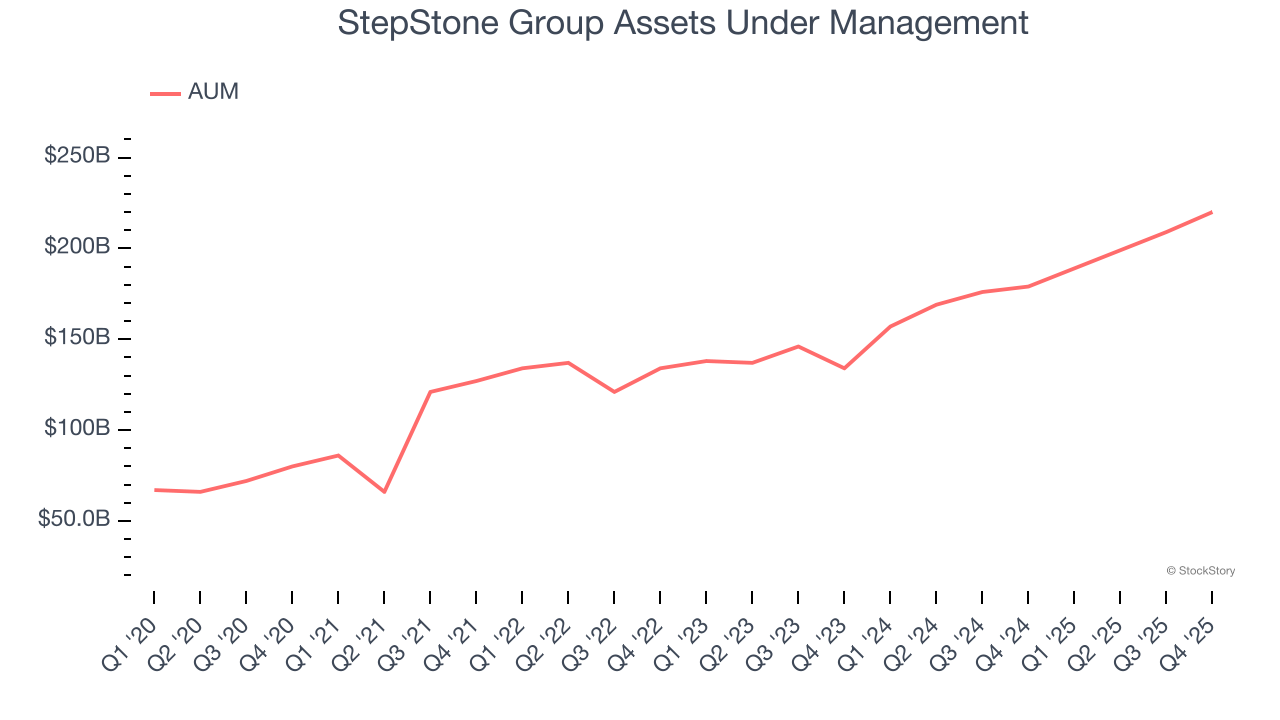

- Assets Under Management: $220 billion vs analyst estimates of $840.5 billion (22.9% year-on-year growth, 73.8% miss)

- Revenue: $586.5 million vs analyst estimates of $418.3 million (140% year-on-year growth, 40.2% beat)

- Pre-tax Profit: -$194.6 million (-33.2% margin)

- Adjusted EPS: $0.65 vs analyst estimates of $0.62 (4.7% beat)

- Market Capitalization: $5.06 billion

Company Overview

Operating as both an advisor and asset manager with over $100 billion in assets under management, StepStone Group (NASDAQ:STEP) is an investment firm that provides clients with access to private market investments across private equity, real estate, private debt, and infrastructure.

Revenue Growth

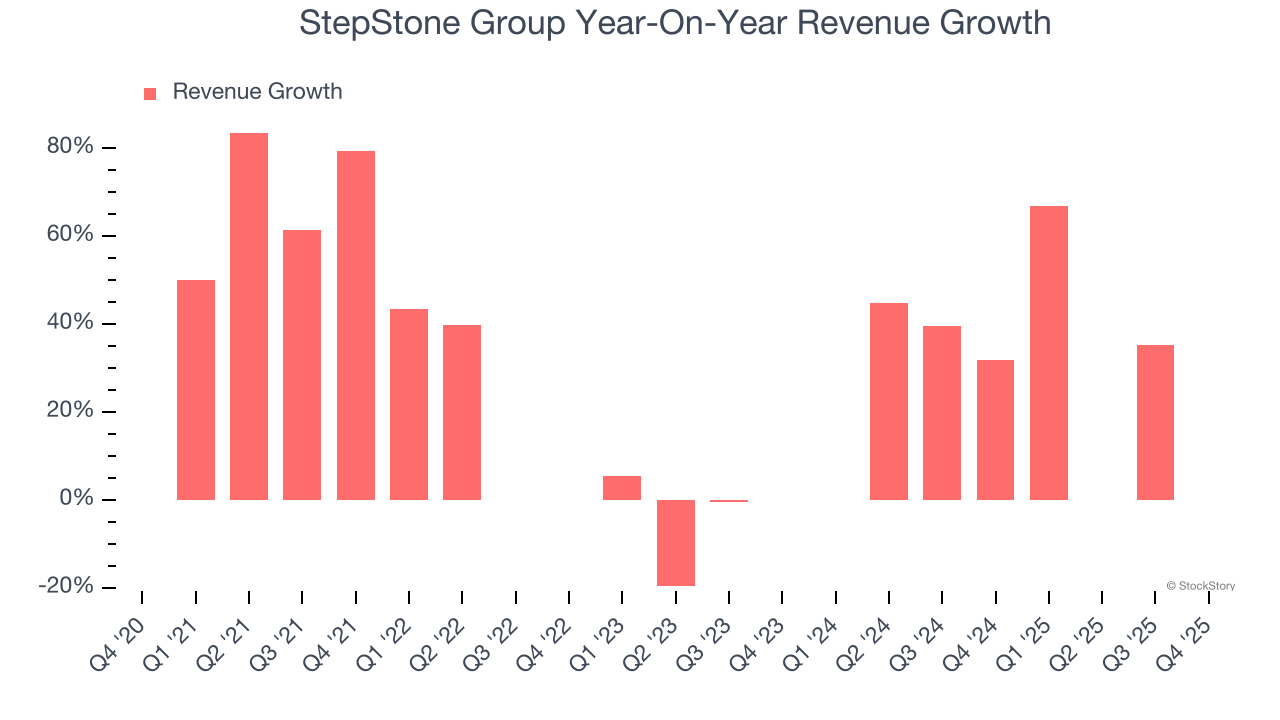

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, StepStone Group’s 34% annualized revenue growth over the last five years was incredible. Its growth surpassed the average financials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. StepStone Group’s annualized revenue growth of 47.9% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, StepStone Group reported magnificent year-on-year revenue growth of 140%, and its $586.5 million of revenue beat Wall Street’s estimates by 40.2%.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Assets Under Management (AUM)

Assets Under Management (AUM) represents the total value of investments that a financial institution manages for its clients. These assets generate steady income through management fees, creating predictable revenue streams that remain stable so long as clients remain invested with the firm.

StepStone Group’s AUM has grown at an annual rate of 23.4% over the last five years, much better than the broader financials industry but slower than its total revenue. When analyzing StepStone Group’s AUM over the last two years, we can see that growth decelerated to 21.3% annually. Fundraising or short-term investment performance were net detractors to the company over this shorter period since assets grew slower than total revenue. That said, assets aren't the be-all and end-all due to their unpredictable and cyclical nature.

StepStone Group’s AUM punched in at $220 billion this quarter, falling 73.8% short of analysts’ expectations. This print was 22.9% higher than the same quarter last year.

Key Takeaways from StepStone Group’s Q4 Results

We were impressed by how significantly StepStone Group blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its AUM missed. Zooming out, we think this was a solid print. The stock remained flat at $59.04 immediately after reporting.

Should you buy the stock or not? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).